[ad_1]

The euro recouped some of last week’s losses, rising 0.25% to $1.0836, adding to its 4.4% gain against the dollar this month. The shared currency had reached $1.0955 last week—its highest since early October—bolstered by Germany’s move to loosen fiscal constraints for military and infrastructure spending. Meanwhile, the Japanese yen edged lower against the greenback as U.S. Treasury yields increased, with the dollar gaining 0.16% to 149.545 yen.

Economic Indicators Show Mixed Signals

Euro zone business activity grew at its fastest pace in seven months in March, supported by an easing in the manufacturing downturn despite slower growth in services.

In the U.S., S&P Global’s flash services index delivered a reading of 54.3 in March, up from 51 in February and exceeding the 51.5 forecast. However, manufacturing fell to 49.8, down from 52.7 and below the expected 51.5. S&P noted that input price inflation accelerated sharply, especially in manufacturing, reaching a near two-year high often attributed to tariff policies.

Market Outlook

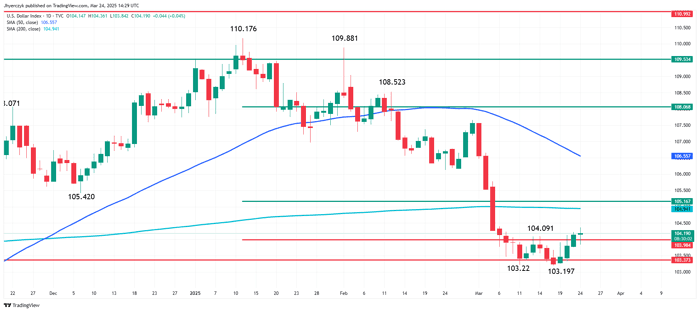

If upside momentum continues, the Dollar Index could surge toward the critical 200-day moving average at 104.941, which currently controls the market’s long-term direction.

However, traders should prepare for continued volatility ahead of the April 2 tariff announcement. The dollar’s performance remains tied to policy clarity, with its year-to-date pressure reflecting the market’s transformation from expectations of pro-growth policies to concerns that aggressive trade measures could trigger economic contraction.

More Information in our Economic Calendar.

[ad_2]